Borrowing money through a loan is a common way to finance big purchases or needs, like a car, home improvements, or starting a business. However, loans come with commitments that can affect your finances for years. Estimating your monthly payments before you borrow is a key step to make sure you can handle the costs without stress.

By calculating payments in advance, you can see if the loan fits your budget. It helps you avoid borrowing more than you need or getting stuck with high costs that lead to financial trouble. For example, if your estimated payment is too high, you might choose a smaller loan or shop for better terms. This process builds confidence and promotes responsible borrowing. In this article, we’ll explain the basics in simple terms, with practical examples to help you get started.

Understanding How Monthly Payments Are Calculated

Monthly loan payments are the amount you pay each month to repay what you borrowed plus the cost of borrowing. This cost is called interest. Payments typically cover both the original amount (principal) and interest.

To estimate payments, use a formula that considers the principal, interest rate, and how long the loan lasts. The standard formula for fixed payments is:

Monthly Payment = Principal × [monthly rate × (1 + monthly rate)^number of months] / [(1 + monthly rate)^number of months – 1]

Don’t worry if this looks complex— we’ll break it down with examples. You can also use online tools or spreadsheets to do the math automatically.

The Relationship Between Loan Amount, Interest Rate, and Loan Duration

Three main factors determine your monthly payment: the loan amount (principal), the interest rate, and the loan duration (term).

- Loan Amount: This is how much you borrow. A larger amount means higher payments because you’re repaying more money.

- Interest Rate: Expressed as a percentage, this is the fee for borrowing. Higher rates increase payments since more of your money goes to interest.

- Loan Duration: The time to repay, usually in years. Shorter terms mean higher monthly payments but less total interest. Longer terms lower monthly payments but raise overall costs.

These elements work together. For instance, a high interest rate on a large loan with a short term results in very high payments. Balancing them helps find affordable options.

What Is Amortization? A Simple Explanation

Amortization is how your loan payments are divided over time. Each payment covers interest and reduces the principal. Early in the loan, more goes to interest because the balance is high. As you pay down the principal, interest decreases, and more of each payment reduces the balance.

This creates a schedule showing the breakdown month by month. It helps you see progress and total interest paid.

For example, on a $10,000 loan at 5% interest for 3 years, the monthly payment is $299.71. Here’s the first three months:

| Month | Payment | Interest | Principal | Balance |

|---|---|---|---|---|

| 1 | $299.71 | $41.67 | $258.04 | $9,741.96 |

| 2 | $299.71 | $40.59 | $259.12 | $9,482.84 |

| 3 | $299.71 | $39.51 | $260.20 | $9,222.64 |

Over time, interest drops, and principal payments rise until the loan is paid off.

Step-by-Step Examples with Easy Numbers

Let’s walk through calculations using simple numbers and real-life scenarios. We’ll use the formula step by step.

Basic Example: A Small Personal Loan

Suppose you need a $5,000 personal loan for home repairs. Current average rates are around 12.15% for good credit. We’ll use 12% for this example, over 2 years.

- Principal (P) = $5,000

- Annual interest rate = 12%, so monthly rate (r) = 0.12 / 12 = 0.01

- Term = 2 years, so number of months (n) = 24

- Calculate (1 + r)^n = (1.01)^24 ≈ 1.2697

- Monthly payment = $5,000 × [0.01 × 1.2697] / [1.2697 – 1] ≈ $5,000 × 0.012697 / 0.2697 ≈ $5,000 × 0.04707 ≈ $235.37

Your monthly payment is about $235. Personal loans like this are unsecured, so rates can be higher, but they’re flexible for various needs.

Real-Life Example: A Car Loan

For a $20,000 new car loan at an average rate of 6.98%, rounded to 7%, over 5 years.

- P = $20,000

- r = 0.07 / 12 ≈ 0.005833

- n = 60

- (1 + r)^n ≈ 1.4177

- Payment = $20,000 × [0.005833 × 1.4177] / [1.4177 – 1] ≈ $20,000 × 0.00827 / 0.4177 ≈ $20,000 × 0.0198 ≈ $396.02

Monthly payments of $396 fit many budgets for reliable transportation.

Real-Life Example: A Small Business Loan

Imagine borrowing $50,000 for business equipment at 10% (common for SBA loans), over 7 years.

- P = $50,000

- r = 0.10 / 12 ≈ 0.008333

- n = 84

- (1 + r)^n ≈ 2.007

- Payment = $50,000 × [0.008333 × 2.007] / [2.007 – 1] ≈ $50,000 × 0.01672 / 1.007 ≈ $50,000 × 0.0166 ≈ $830.06

This helps businesses grow while managing cash flow.

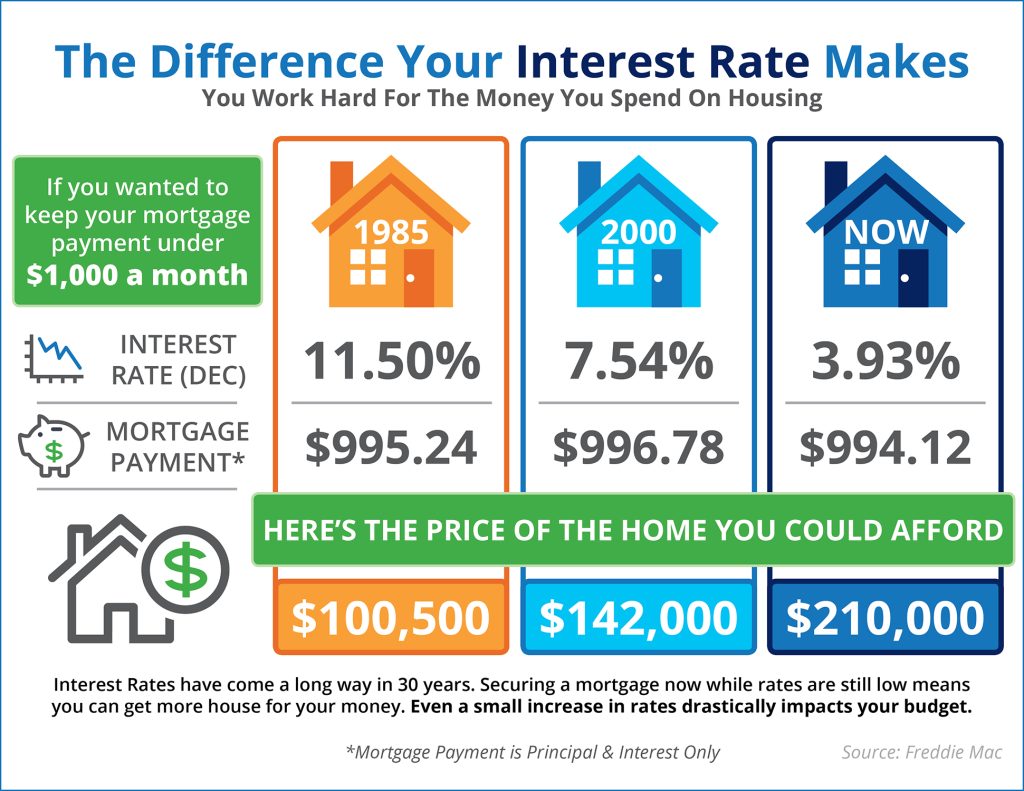

How Changing Interest Rates Affects Monthly Payments: A Comparison

Interest rates greatly influence payments. Even small changes add up.

Compare a $15,000 loan over 3 years at different rates:

| Interest Rate | Monthly Payment |

|---|---|

| 5% | $449.56 |

| 7% | $463.16 |

| 9% | $477.00 |

At 5%, you pay $449 monthly. At 9%, it’s $477— an extra $27 per month, or over $900 more in total interest. Shop for lower rates by improving credit or comparing lenders.

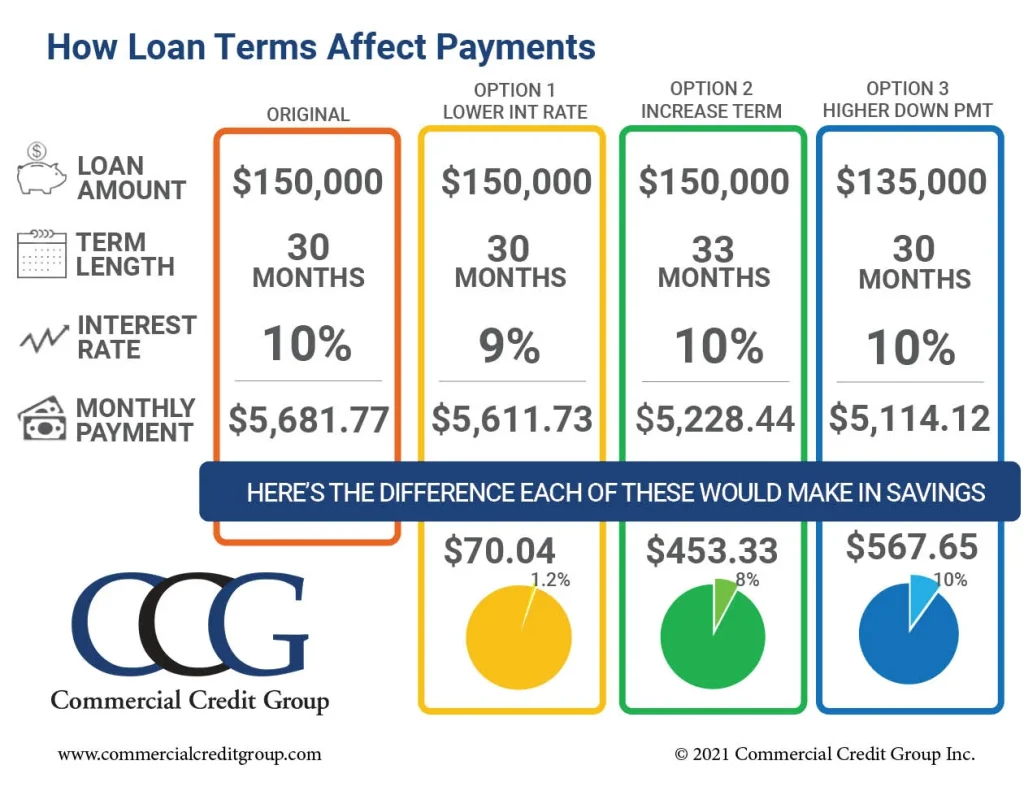

How Changing Loan Duration Affects Monthly Payments: A Comparison

Loan term affects affordability and total cost.

For a $15,000 loan at 6%:

| Term (Years) | Monthly Payment | Total Interest |

|---|---|---|

| 3 | $456.33 | $1,427.88 |

| 5 | $289.99 | $2,399.40 |

| 7 | $219.13 | $3,406.92 |

Shorter terms save on interest but require higher payments. Longer terms ease monthly burdens but cost more overall.

Fixed vs. Variable Rates: Impact on Monthly Payments

Fixed rates stay the same, so payments are predictable. Variable rates change with market conditions, potentially lowering or raising payments.

Fixed rates suit stable budgets; if rates are low, like current car loans at 6.98%, lock in. Variable rates might start lower but risk increases— e.g., a 5% variable could rise to 8%, bumping payments from $449 to $469 on a $15,000, 3-year loan.

Choose based on risk tolerance and economic outlook.

Common Mistakes When Estimating Repayments

People often overlook fees, like origination costs, which add to the effective rate. Another error is ignoring credit impact— poor credit means higher rates, like 14.48% for personal loans.

Miscalculating terms or rates leads to surprises. Always double-check with tools and include all costs.

Practical Tips to Avoid Overborrowing

- Assess needs: Borrow only what you require.

- Budget check: Payments should be under 20-30% of income.

- Compare offers: Look at APR for true costs.

- Build credit: Better scores get lower rates.

- Use tools: Try our Loan Calculator tool to test scenarios.

These steps prevent debt overload.

Summary: Key Takeaways

Estimating monthly loan payments helps you borrow smartly. Remember the roles of principal, rate, and term; understand amortization; and compare options. Avoid common pitfalls and use tips to stay in control. With this knowledge, you’ll make informed decisions for a healthier financial future.