Taking out a loan is a big step in managing your finances. Whether you’re buying a car, starting a small business, or covering unexpected expenses, borrowing money means committing to regular payments over time. But before you sign any papers, it’s essential to figure out exactly what those payments will look like. Calculating loan repayments in advance helps you understand if you can afford the loan without stretching your budget too thin.

Imagine applying for a loan and only finding out later that the monthly payments are higher than expected. This could lead to stress, missed payments, or even damage to your credit score. By doing the math upfront, you gain control. You can compare different loan options, spot better deals, and avoid surprises. This simple habit promotes smarter financial decisions and reduces the risk of debt overload. In this article, we’ll break down the process in easy steps, using clear examples to make it accessible for beginners.

What Makes Up a Loan Repayment?

At its core, a loan repayment is made up of two main parts: the principal and the interest. The principal is the original amount of money you borrow. For example, if you take out a $10,000 loan, that’s your principal. Over time, your payments chip away at this amount until it’s fully paid back.

The interest is the extra cost the lender charges for letting you use their money. It’s like a fee for borrowing. Interest is calculated as a percentage of the principal and added to your repayments. So, if your loan has a 5% interest rate, you’re paying an additional 5% on the borrowed amount over the loan’s life.

Together, principal and interest form your total repayment. Early on, more of your payment might go toward interest, but as you pay down the principal, that shifts. This process is called amortization, which we’ll explore more later. Understanding these basics helps you see why loans cost more than just the amount borrowed—sometimes a lot more, depending on the terms.

Understanding Interest Rates and How They Affect Total Repayment

Interest rates are a key factor in any loan. They represent the cost of borrowing, shown as a percentage. A lower rate means less extra cost; a higher rate means more. For instance, on a $10,000 loan at 5% interest over three years, you might pay around $800 in interest total. But at 10%, that could jump to over $1,600.

Rates are influenced by things like your credit history, the economy, and the lender. In February 2026, average personal loan rates are around 12-14% for good credit borrowers. For small business loans, they range from 7-11% at banks or up to 14% for SBA options. These figures can change, so always check current rates.

The impact on total repayment is significant. Higher rates increase your monthly payments and the overall amount paid. To illustrate, consider two $20,000 loans over five years: one at 6% (total repayment about $23,200) versus one at 12% (around $26,700). That’s an extra $3,500 just from the rate difference. Always factor in how rates add up over time to avoid paying more than necessary.

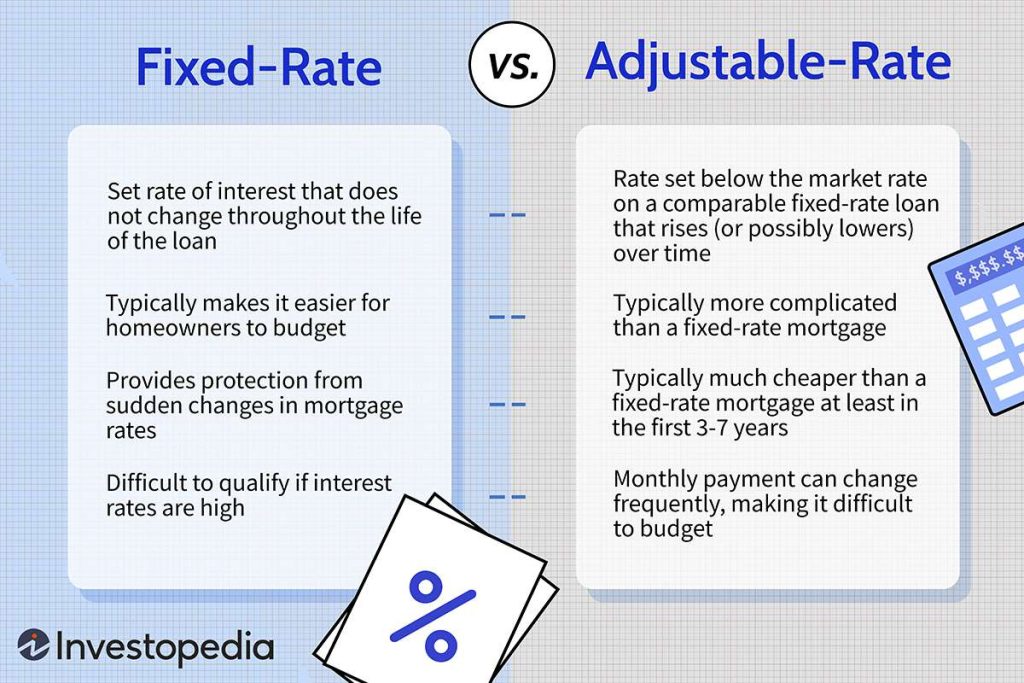

The Difference Between Fixed and Variable Interest Rates

When choosing a loan, you’ll encounter fixed and variable interest rates. A fixed rate stays the same throughout the loan term. If you lock in at 6%, your payments remain predictable, making budgeting easier. This is great for stability, especially if rates are low when you borrow.

A variable rate, on the other hand, can change based on market conditions. It might start lower than a fixed rate—say, 5% initially—but could rise to 8% or more if interest rates go up. This means your payments could increase, adding uncertainty. However, if rates drop, you might save money.

The choice depends on your situation. Fixed rates suit those who want consistency, like first-time borrowers. Variable rates might appeal if you expect rates to fall or plan to pay off the loan quickly. Remember, variable options can lead to higher costs if rates rise unexpectedly.

The Role of Loan Duration and How It Impacts Total Cost

Loan duration, or term, is how long you have to repay the loan—often in months or years. Shorter terms, like three years, mean higher monthly payments but less total interest. Longer terms, such as ten years, lower monthly payments but increase overall costs due to more interest accruing.

For example, a $50,000 loan at 4% interest: Over 10 years, monthly payments are about $506, with total interest around $10,750. Shorten it to five years, and payments rise to $922, but interest drops to about $5,300. The trade-off is affordability versus total expense.

Longer durations can make loans seem cheaper monthly, but they cost more in the end. Always balance what you can pay now with the long-term price. Shorter terms save money if your budget allows.

Step-by-Step Guide to Calculating Loan Repayments

Calculating repayments isn’t as hard as it seems. We’ll use a simple formula for fixed-rate loans:

Monthly Payment (M) = P × [r(1 + r)^n] / [(1 + r)^n – 1]

Where:

- P is the principal

- r is the monthly interest rate (annual rate / 12)

- n is the number of months (years × 12)

Step 1: Gather details. Say, principal $10,000, annual rate 5%, term 3 years.

Step 2: Convert to monthly. r = 5% / 12 = 0.004167, n = 36.

Step 3: Calculate (1 + r)^n = about 1.1616.

Step 4: Numerator = r × 1.1616 ≈ 0.004841.

Step 5: Denominator = 1.1616 – 1 = 0.1616.

Step 6: M = 10,000 × (0.004841 / 0.1616) ≈ $299.71.

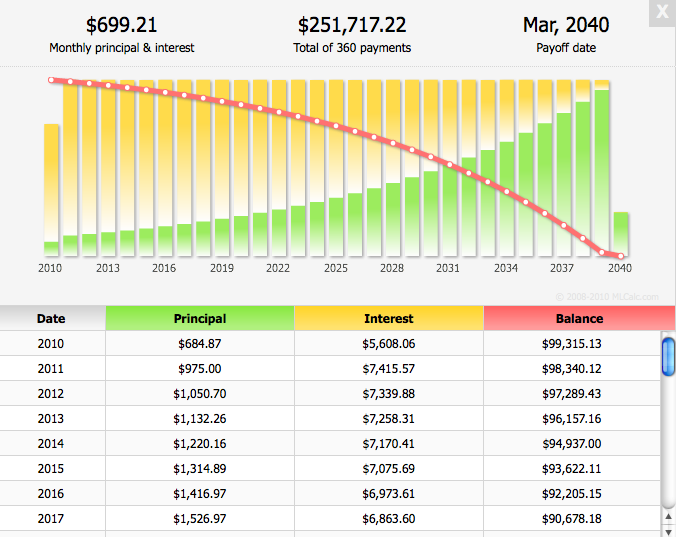

This covers principal and interest. For a full picture, create an amortization table showing how payments split over time.

Here’s a sample for the first few months of our $10,000 loan:

| Month | Payment | Interest | Principal | Remaining Balance |

|---|---|---|---|---|

| 1 | $299.71 | $41.67 | $258.04 | $9,741.96 |

| 2 | $299.71 | $40.59 | $259.12 | $9,482.84 |

| 3 | $299.71 | $39.51 | $260.20 | $9,222.64 |

| 4 | $299.71 | $38.43 | $261.28 | $8,961.36 |

| 5 | $299.71 | $37.34 | $262.37 | $8,698.99 |

Notice interest decreases as principal shrinks.

Try another: $20,000 at 6% for 5 years. Monthly payment: $386.66. Total paid: about $23,200.

Real-Life Examples: Personal Loans and Small Business Loans

Let’s apply this to everyday scenarios. For a personal loan, suppose you need $10,000 for home repairs. With average rates at 12% in 2026, over 3 years: r = 0.01, n=36. Payment ≈ $332.14. Total interest: about $1,957.

If your credit is good (score 690+), you might get 14.48%, making payments $345. Total: $12,420.

For a small business loan, say $50,000 for equipment at 10% (common for SBA loans), over 10 years: Payment ≈ $660.75. Total interest: $29,290.

Shorter term (5 years): Payment $1,060.66, interest $13,640. Business owners should weigh cash flow against savings.

These examples show how terms affect real costs. Adjust based on your rates.

How to Estimate Your Monthly Payments

Estimating payments is straightforward with tools or math. Use the formula above for manual calc, or online calculators for speed.

Input principal, rate, and term; it spits out the monthly amount. For accuracy, include fees.

Check out our Loan Calculator page for quick estimates. It’s free and helps visualize scenarios.

Spreadsheets like Excel use =PMT(rate, periods, principal). Example: =PMT(0.05/12, 36, -10000) gives $299.71.

Practice with different numbers to see changes.

Watch Out for Hidden Charges and Extra Fees

Loans often have extras beyond principal and interest. Origination fees (1-6% of loan) add upfront costs. Late fees penalize missed payments. Prepayment penalties charge for early payoff.

For example, a 2% origination on $10,000 adds $200, effectively raising your rate. Always read fine print. Ask lenders to disclose all fees. Factor them into calculations for true cost.

Taxes or insurance (e.g., on car loans) can also add up. Ignoring these leads to underestimating expenses.

Practical Tips for Comparing Loan Offers

To find the best deal:

- Shop multiple lenders: Compare rates, terms, fees.

- Check APR: Includes fees for true comparison.

- Use debt-to-income ratio: Ensure payments <36% of income.

- Improve credit: Higher score = lower rates.

- Consider co-signers for better terms.

- Read reviews: Avoid lenders with poor service.

Run calculations for each offer. A lower rate might beat shorter term if fees are high.

Conclusion: Key Takeaways for Smart Borrowing

Calculating loan repayments empowers you to borrow wisely. Remember: Repayments include principal and interest; rates and terms greatly affect costs; fixed offers stability, variable potential savings; watch for fees.

By following steps and using tools like our Loan Calculator, you’ll make informed choices. Start small with examples, and always align with your budget. This knowledge builds financial confidence for the future.